Third Quarter 2024: The Eagle Just Might Be Landing

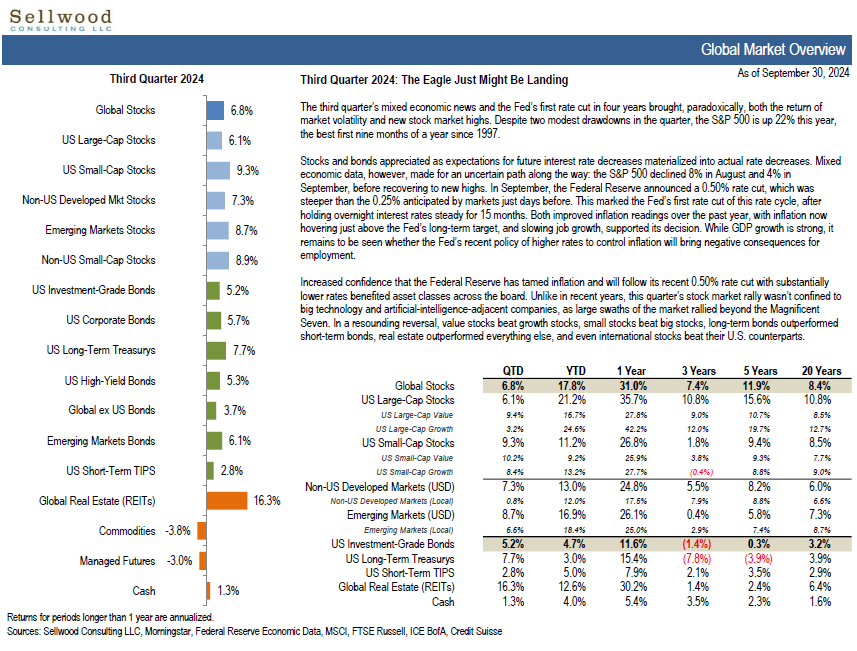

The third quarter’s mixed economic news and the Fed’s first rate cut in four years brought, paradoxically, both the return of market volatility and new stock market highs. Despite two modest drawdowns in the quarter, the S&P 500 is up 22% this year, the best first nine months of a year since 1997.

Stocks and bonds appreciated as expectations for future interest rate decreases materialized into actual rate decreases. Mixed economic data, however, made for an uncertain path along the way: the S&P 500 declined 8% in August and 4% in September, before recovering to new highs. In September, the Federal Reserve announced a 0.50% rate cut, which was steeper than the 0.25% anticipated by markets just days before. This marked the Fed’s first rate cut of this rate cycle, after holding overnight interest rates steady for 15 months. Both improved inflation readings over the past year, with inflation now hovering just above the Fed’s long-term target, and slowing job growth, supported its decision. While GDP growth is strong, it remains to be seen whether the Fed’s recent policy of higher rates to control inflation will bring negative consequences for employment.

Increased confidence that the Federal Reserve has tamed inflation and will follow its recent 0.50% rate cut with substantially lower rates benefited asset classes across the board. Unlike in recent years, this quarter’s stock market rally wasn’t confined to big technology and artificial-intelligence-adjacent companies, as large swaths of the market rallied beyond the Magnificent Seven. In a resounding reversal, value stocks beat growth stocks, small stocks beat big stocks, long-term bonds outperformed short-term bonds, real estate outperformed everything else, and even international stocks beat their U.S. counterparts.